Understanding “Buy Now Pay Later”

Buy Now Pay Later (BNPL) is a payment method that has become increasingly popular recently. It allows consumers to purchase items without paying the full amount upfront and instead spread the cost over a period of time.

What is Buy Now Pay Later?

Buy Now Pay Later is a payment method that allows customers to purchase items and pay for them in installments, typically throughout 6 to 12 months. This payment method is popular among online retailers and e-commerce platforms like Amazon, Walmart, and Best Buy. BNPL services are usually offered by third-party providers, such as Klarna, Afterpay, and Affirm.

Visa/ Facebook | BNPL services are popular among millennials and Gen Z consumers

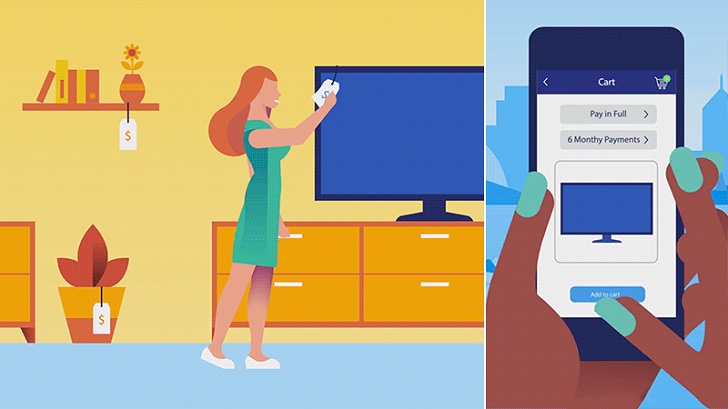

How Does BNPL Work?

When customers select BNPL as a payment option, they are typically required to provide basic personal information, such as their name, address, and date of birth. They may also be asked to provide their employment details and income. Once the customer’s information is verified, they can pay for their purchase in installments over a set period, usually 2 to 12 months.

Benefits of BNPL

One of the main benefits of BNPL is that it allows consumers to purchase items without paying the full amount upfront. This can be particularly useful for those on a tight budget or who cannot afford to pay for large purchases in one go. BNPL can also be a good option for those who want to spread the cost of a purchase over a longer period of time.

Another benefit of BNPL is that it can help to improve credit scores. This is because when a customer uses BNPL and makes regular payments, it shows that they are responsible with their finances and can make payments on time. This can help to improve their credit score over time.

Pixabay/ Pexels | There were 360 million BNPL users worldwide in 2022

Drawbacks of BNPL

While BNPL can be a useful payment option for some, it has some drawbacks. One of the main drawbacks is that it can encourage consumers to spend more money than they can afford. This is because BNPL makes it easy for consumers to purchase without paying the full amount upfront. As a result, consumers may be tempted to make purchases they cannot afford to pay back in full.

Another drawback of BNPL is that it can be expensive. Many BNPL providers charge interest rates, which can be higher than traditional credit cards. This means that if consumers cannot pay back their BNPL payments on time, they may pay significant interest charges.

Oscar Wong/ Moment | Getty Images | As BNPL continues to grow in popularity, retailers and other organizations that do not have this option could fall behind

Future Outlook of BNPL

The future of BNPL looks bright, with the payment method continuing to gain popularity among consumers, according to a report by Worldpay, the global BNPL market is set to grow by 46% between 2020 and 2025, reaching a value of $995 billion. This growth is expected to be driven by increasing consumer demand for alternative payment options, particularly among younger consumers.

In addition, many traditional lenders and credit card providers are starting to offer BNPL services to compete with third-party providers. This will likely drive further growth in the BNPL market and increase provider competition.

More in Legal Advice

-

`

Santo Spirits: Sammy Hagar and Guy Fieri’s Joint Venture

Santo Spirits: Sammy Hagar and Guy Fieri’s Joint VentureIn the world of business partnerships, some combinations might seem unconventional at first glance. But when you delve deeper into the...

November 16, 2023 -

`

Everything You Need to Know About Mortgage Rate Lock

Everything You Need to Know About Mortgage Rate LockYou have probably embarked on the exciting yet nerve-wracking voyage of purchasing a home. Amidst the sea of paperwork, open houses,...

November 9, 2023 -

`

7 Effective Ways to Make Your Business More Sustainable

7 Effective Ways to Make Your Business More SustainableIn an age of rising environmental consciousness, making your business more sustainable isn’t just a trend; it’s a necessity. Sustainable practices...

November 3, 2023 -

`

Housing Market Going Up? Then Why Not Rent?

Housing Market Going Up? Then Why Not Rent?“Buy a house! It is the best investment!” How many times have you heard that? Probably enough to make a drinking...

October 29, 2023 -

`

Surprising! Celebs Who You Didn’t Know Had a Master’s Degree

Surprising! Celebs Who You Didn’t Know Had a Master’s DegreeWhen it comes to celebrities, we often associate them with glitz, glamour, and blockbuster movies. But did you know that some...

October 17, 2023 -

`

Navigating the Housing Maze: The 7% Mortgage Rate Quandary

Navigating the Housing Maze: The 7% Mortgage Rate QuandaryIf there is one thing that this year has thrown our way (apart from those fascinating tech gadgets we did not know...

October 12, 2023 -

`

Where to Buy a House in the U.S With a $100K Salary

Where to Buy a House in the U.S With a $100K SalaryGot a cool $100,000 annual paycheck in your pocket? Cheers to that accomplishment! With such a financial cushion, dreams of homeownership...

October 6, 2023 -

`

The “Grave” Housing Crisis Forcing U.S. Homeowners to Sell Their Houses

The “Grave” Housing Crisis Forcing U.S. Homeowners to Sell Their HousesEvery culture has its dreams and aspirations. For those living in the United States, it has traditionally been an idyllic house, spacious and...

October 1, 2023 -

`

Why Private Equity is Betting Big on Hollywood

Why Private Equity is Betting Big on HollywoodHollywood has long been a glamorous yet unpredictable industry. But what is new in Tinseltown? Private equity investments. Yes, that is right!...

September 19, 2023

More From MortgageAfterLife

-

Who Is Dwayne Johnson Married To? The Love Story That Will Make You Swoon

Who Is Dwayne Johnson Married To? The Love Story That Will Make You SwoonThe heartwarming tale of Dwayne “The Rock” Johnson and Lauren Hashian is a true testament to the power of love, overcoming...

Star AdvisorApril 11, 2024 -

Boat Interest Rates Too High? Here’s How to Score a Better Deal

Boat Interest Rates Too High? Here’s How to Score a Better DealAre you dreaming of setting sail into the sunset but daunted by the prospect of financing your maritime adventure? You’re not...

Pocket ChangeApril 6, 2024 -

Antitrust Hurdles Stop the Spirit Airlines JetBlue Merger in Its $3.8 Billion Tracks

Antitrust Hurdles Stop the Spirit Airlines JetBlue Merger in Its $3.8 Billion TracksIn what turned out to be a dramatic turn of events for the aviation industry, the proposed $3.8-billion Spirit Airlines JetBlue...

Finance & BusinessMarch 31, 2024 -

“Shakedown” or Truth? McSweeney Fires Back at Cohen After Lawsuit Denial

“Shakedown” or Truth? McSweeney Fires Back at Cohen After Lawsuit DenialThe Brewing Storm The legal battle between U.S. television network Bravo and former “Real Housewives of New York City” star Leah...

Legal AdviceMarch 20, 2024 -

Entrepreneurship 101: How Miguel’s Artisan Recipes Expanded From a Pop-up Store to a Complete Storefront

Entrepreneurship 101: How Miguel’s Artisan Recipes Expanded From a Pop-up Store to a Complete StorefrontIn the heart of California, a local Mexican homemade dish has been capturing hearts and palates for decades. Miguel’s Artisan Recipes,...

Finance & BusinessMarch 16, 2024

You must be logged in to post a comment Login